Taking a loan is one of the biggest financial decisions most people make. Whether it's a home loan of ₹40 lakh, a car loan of ₹8 lakh, or a personal loan of ₹3 lakh to handle an urgent expense, one number shapes your life for years — your monthly EMI. Yet most people learn that number from a bank executive and accept it without questioning whether a different tenure or loan amount might have served them better.

This guide walks you through exactly how to calculate EMI online using a free EMI calculator, what the result actually means, how to read an amortization schedule, and what practical decisions you can make with that information before you sign the loan agreement.

What Is an EMI and How Is It Calculated?

EMI stands for Equated Monthly Installment. It is the fixed amount you pay your lender every month until the loan is fully repaid. The word "equated" is important — your monthly payment stays the same throughout the loan tenure, but the split between interest and principal changes with every payment.

In the early months of any loan, most of your EMI goes toward paying interest on the outstanding balance. A small portion actually reduces the principal. As the outstanding balance decreases month by month, the interest component shrinks and the principal component grows. By the last few months, almost your entire EMI is principal repayment. This structure is called the reducing balance method and it is the standard used by every bank and NBFC in India for home loans, car loans, and personal loans.

The formula banks use is:

EMI = P × r × (1 + r)^n ÷ [(1 + r)^n − 1]

P is the principal loan amount. r is the monthly interest rate, calculated by dividing the annual rate by 12 and then by 100. n is the loan tenure in months.

You don't need to use this formula manually. A free online EMI calculator does the computation instantly — and more importantly, it also generates the full loan repayment schedule so you can see every month of the loan at a glance.

How to Calculate EMI Online — Step by Step

Using the EzyToolz free EMI calculator takes about thirty seconds. Here is exactly what to do.

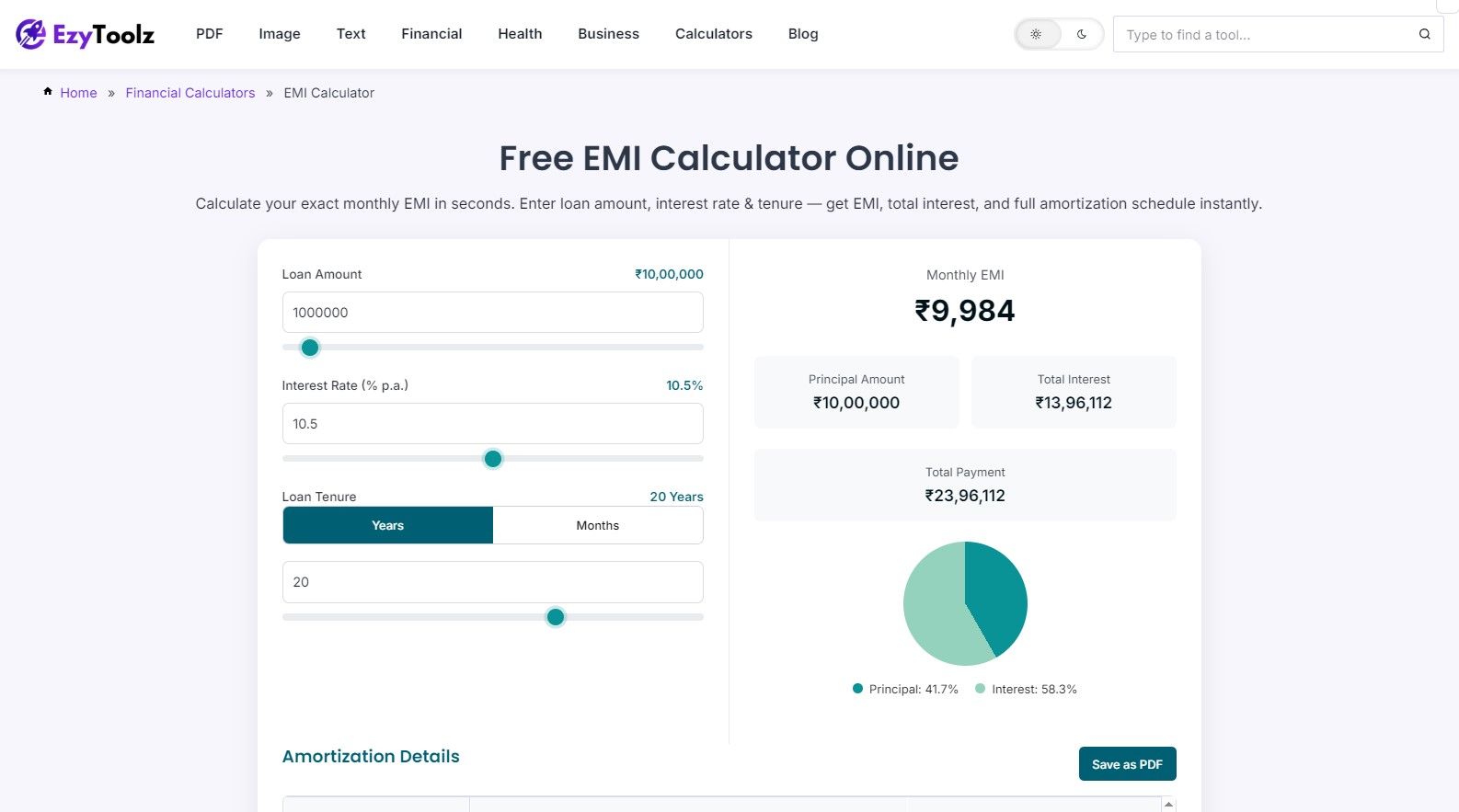

Step 1 — Open the EMI calculator. Go to the EzyToolz EMI Calculator page. You'll see three input fields: Loan Amount, Interest Rate, and Loan Tenure. There are also sliders for each field if you prefer to adjust values visually.

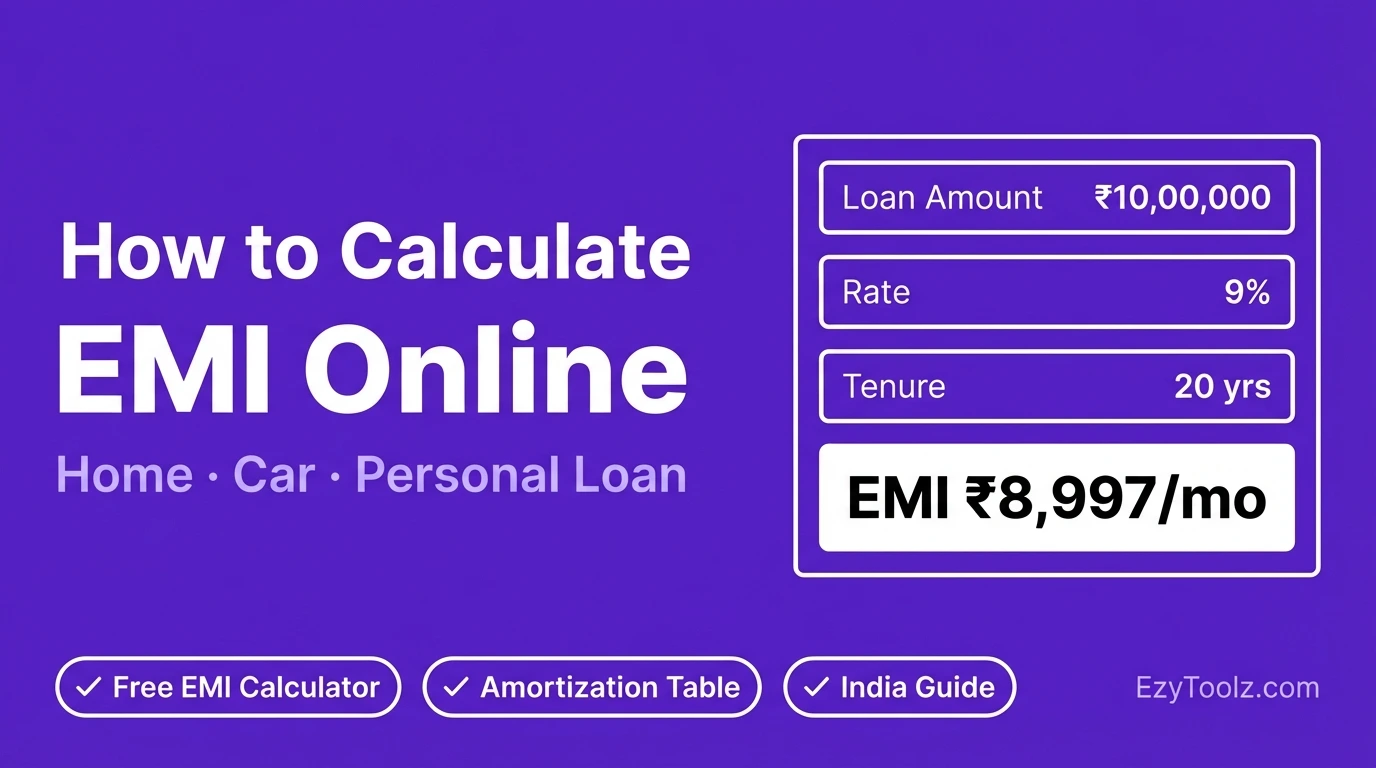

Step 2 — Enter your loan amount. Type the amount you plan to borrow. For a home loan this might be ₹25 lakh, ₹40 lakh, or ₹60 lakh. For a car loan it could be ₹6 lakh to ₹15 lakh. For a personal loan, enter the exact amount you need — even ₹50,000 upward works with this monthly EMI calculator.

Step 3 — Set the interest rate. Enter the annual interest rate your bank has quoted. For home loans in India, rates in 2026 range from around 8.40% at public sector banks for high-credit borrowers to 10.5% or above at NBFCs. Car loan rates typically fall between 7.5% and 14%. Personal loan rates are higher — commonly 10.5% to 22% depending on your lender and CIBIL score. Use the exact figure from your loan offer letter for the most accurate EMI calculation.

Step 4 — Choose your tenure. Enter the loan term. Use the Years/Months toggle to switch between the two. Home loans commonly run 10 to 30 years. Car loans are usually 3 to 7 years. Personal loans range from 1 to 5 years. Try a few different tenures here — the monthly EMI calculator updates instantly, so you can immediately compare what a 15-year tenure costs versus a 20-year tenure for the same loan.

Step 5 — Read your results. The calculator instantly shows your monthly EMI, total principal, total interest payable, and combined total payment. The pie chart gives you a visual split — on a long home loan, seeing that 55% of your total payment is interest is far more impactful than reading the number alone.

Step 6 — Scroll down to the amortization schedule. This is the most useful part of the entire loan repayment schedule calculator. The table shows every single month of your loan: how much of that month's EMI goes to principal, how much goes to interest, and what your outstanding balance is after that payment. You can also save this as a PDF for reference or to share with a co-borrower.

What the Amortization Schedule Reveals

Most borrowers focus only on the monthly EMI figure. The loan amortization schedule tells a more complete story.

Take a ₹40 lakh home loan at 9% interest for 20 years. The monthly EMI works out to approximately ₹35,989. In the very first month, about ₹30,000 of that EMI is interest and only ₹5,989 reduces the actual balance. After one full year of payments — twelve EMIs totalling roughly ₹4.32 lakh — your outstanding loan balance has barely moved. Over the full 20 years, the total interest you pay is approximately ₹46.37 lakh — more than the principal itself.

This is not a mistake. It is how reducing balance EMI calculation works mathematically. But seeing these numbers in the EMI calculator with amortization schedule changes how you think about prepayment and tenure selection.

If you shorten the same ₹40 lakh loan to 15 years, the EMI rises to approximately ₹40,572 — an increase of ₹4,583 per month. But the total interest drops to about ₹33 lakh, saving you over ₹13 lakh compared to the 20-year option. That ₹4,583 extra per month costs you far less than the ₹13 lakh you avoid paying in interest.

Home Loan, Car Loan, Personal Loan — How EMI Differs

The same EMI formula applies to all three loan types, but the typical numbers look very different.

For a home loan EMI calculation, the large principal and long tenure mean that interest dominates the early years of the repayment schedule. Public sector banks like SBI and Canara Bank tend to offer lower rates than private lenders, especially to borrowers with CIBIL scores above 750. Home loans also come with tax benefits — deductions up to ₹2 lakh on interest under Section 24(b) and up to ₹1.5 lakh on principal under Section 80C — which partially offsets the interest cost.

For a car loan EMI calculation, the shorter tenure and moderate loan amount keep total interest lower in absolute terms, but the interest rate is typically higher than home loans. Comparing the 5-year versus 7-year option in the online loan calculator is especially useful here. On a ₹10 lakh car loan at 9.15%, a 5-year tenure gives an EMI of ₹20,798 with ₹2.48 lakh in total interest. A 7-year tenure lowers the EMI to ₹15,867 but raises total interest to ₹3.33 lakh — ₹85,000 more for two extra years of lower payments.

For a personal loan EMI calculation, the higher interest rates mean even short tenures carry significant interest costs. On a ₹5 lakh personal loan at 14% for 3 years, the EMI is ₹17,087 and total interest is ₹1.15 lakh. Running the same calculation at 18% raises the total interest to ₹1.51 lakh — a difference of ₹36,000 just from a 4-percentage-point rate gap. This makes using a personal loan EMI calculator before accepting any offer one of the simplest ways to save money.

Practical Tips Before You Take the Loan

Before signing, use the free online EMI calculator to run at least three scenarios: the loan amount and tenure the bank has proposed, a shorter tenure to see the interest saving, and a smaller loan amount to see how a larger down payment changes the total cost.

Keep your total EMI commitments — home loan, car loan, and any other borrowings combined — below 40% to 50% of your monthly take-home salary. This is what lenders in India call FOIR (Fixed Obligation to Income Ratio), and staying within it keeps your monthly budget stable and your loan application strong.

If you already have a running loan, the same EMI calculator can help you evaluate prepayment. Enter your remaining balance as the new loan amount, keep the current interest rate and remaining tenure, and compare it against a shorter tenure with the same rate. The difference in total interest shows you exactly what a lump sum prepayment would save.